By using our website, you agree to the use of cookies as described in our Cookie Policy

Blog

Good News, (Potential) Bad News on the Economy

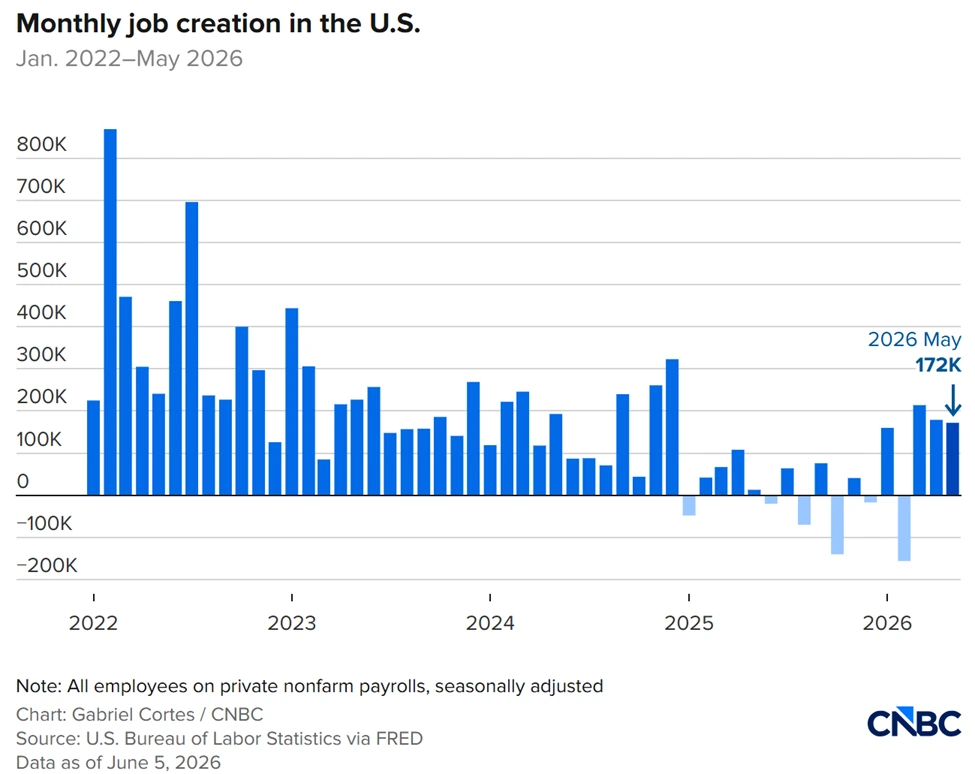

The May jobs report was unexpectedly strong, as nonfarm payrolls grew 172,000, well above the Dow Jones consensus estimate of 80,000. In addition, the April and March reports were revised upward by a combined 93,000 jobs. The low hiring, low firing environment that characterized labor markets in 2025 may have come to an end, as nicely illustrated by this chart from CNBC’s Jeff Cox:

Following the jobs report, the S&P 500 has fallen over 2% as of mid-afternoon. Given that a stronger economy makes rate cuts by the Fed less likely and rate hikes more so, this market reaction is not surprising. Still, average hourly earnings rose only 0.3% for the month and 3.4% over the past year, as expected, so there’s not increased inflationary pressure on that front.

The potential dark clouds over a promising economy are a rise in oil prices, as the stalemate in the Iran war continues. A U.S. blockade of Iranian ports is damaging the Iranian economy, while the near-closure of the Strait of Hormuz is damaging the global economy.

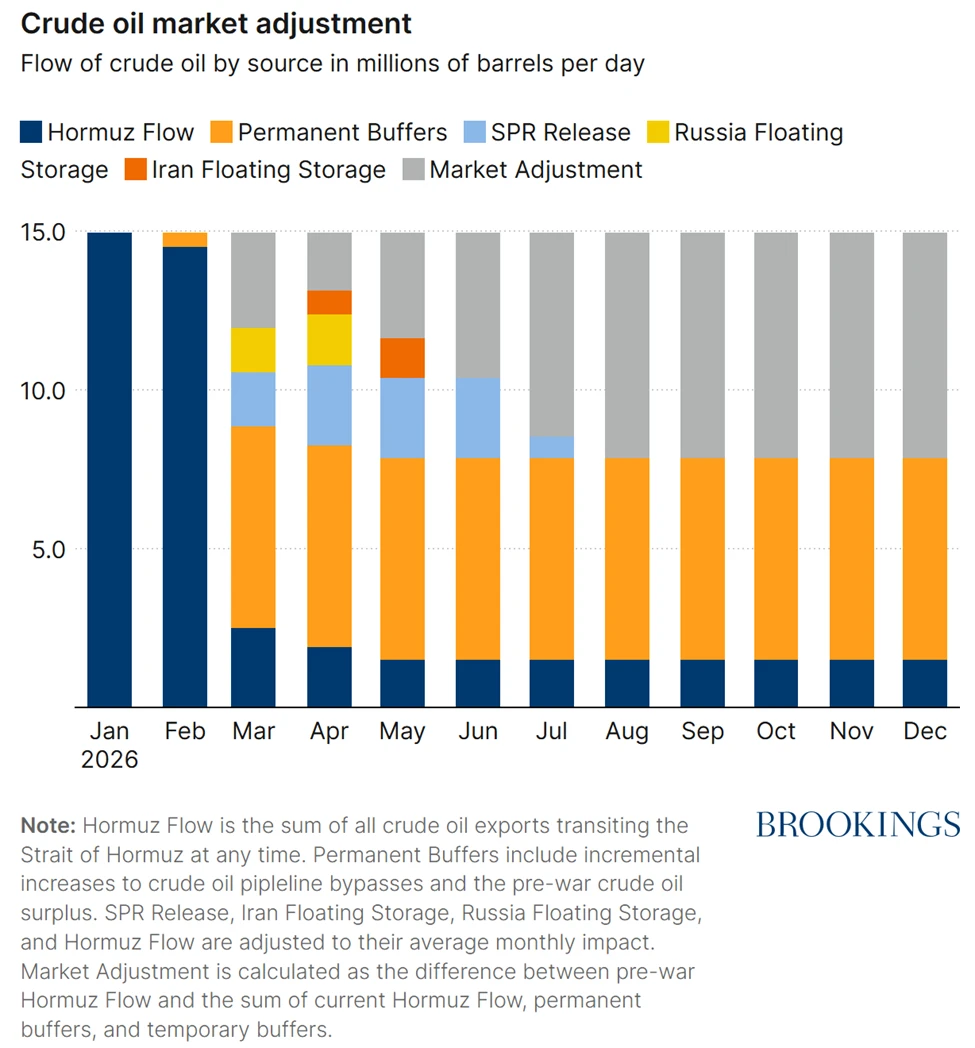

So far, the rise in oil prices from the Iran war have been moderate in scope, at least relative to the rise in oil prices in 2022 following Russia’s invasion of Ukraine. However, Robin Brooks and Ben Harris argue that the clock is ticking—oil price increases have been limited in part by the drawdowns of oil reserves from many sources, but as these stockpiles dwindle, oil prices may spike. The authors provide a useful chart illustrating their estimates:

While increased production elsewhere has provided significant permanent buffers that help to reduce the crude oil shortfall, many temporary measures, such as the U.S. Strategic Petroleum Reserve release, are expected to run out by the end of July. At that point, absent further measures, market adjustments would be needed to cover the 7.1 million barrels per day shortfall, which is about 16% of global crude oil trade. In other words, oil prices would need to rise.

Brooks and Harris suggest a 10% reduction in oil supply from the start of the war until June would result in a Brent crude price of $120 per barrel. The larger reduction in oil supply that would result as temporary oil buffers dissipate would, by the authors’ estimate, yield oil prices nearing $150 per barrel. As of this writing, oil futures have fallen in recent weeks, suggesting that markets believe a deal between the U.S. and Iran will be struck, and an additional oil price spike will be evaded.

JMS Capital Group Wealth Services LLC

417 Thorn Street, Suite 300 | Sewickley, PA | 15143 | 412‐415‐1177 | jmscapitalgroup.com

An SEC‐registered investment advisor.

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument or investment strategy. This material has been prepared for informational purposes only, and is not intended to be or interpreted as a recommendation. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice.

‹ Back

Recent Posts

-

Quarterly Market Commentary

August 4, 2026

-

Good News, (Potential) Bad News on the Economy

June 5, 2026

-

Are There Rising Interest Rates on the Horizon?

May 29, 2026

-

May Charts and Links

May 15, 2026

-

The S&P 500 Has Reconcentrated

May 11, 2026