By using our website, you agree to the use of cookies as described in our Cookie Policy

Blog

The S&P 500 Has Reconcentrated

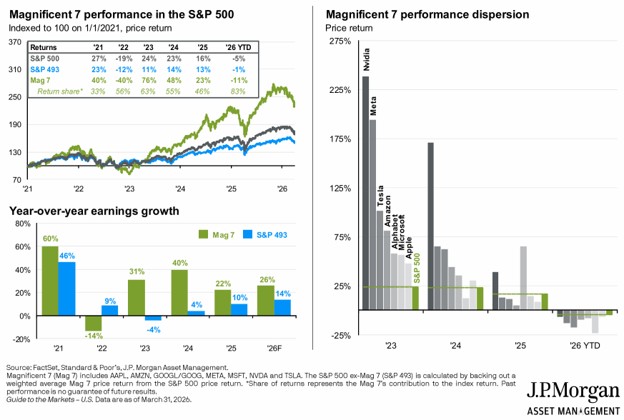

For the past year or so we had seen a broadening of the bull market with respect to the S&P 500. Yes, a handful of tech behemoths was still leading the way, but price appreciation was nonetheless widespread:

From 2023 to 2025 the S&P 493 (the S&P 500 excluding Apple, Amazon, Google, Meta, Microsoft, Nvidia, and Tesla) had returns of 11%, 14%, and 13%, respectively. By 2025, the Mag 7’s surge had slowed somewhat, returning ‘only’ 23% in that year. Strong Mag 7 earnings growth, as shown above, provided an increasing justification for the Mag 7’s stock price surge.

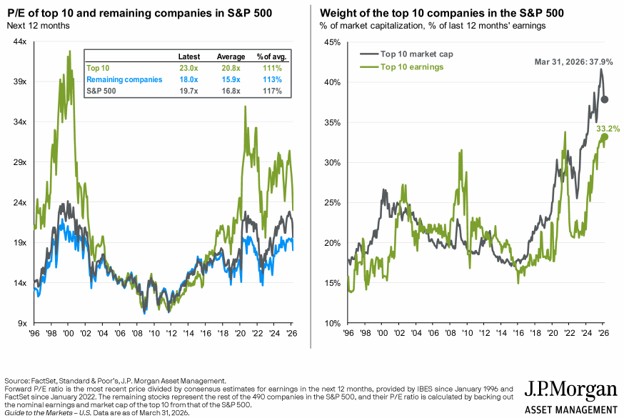

As of March 31st, P/E ratios for the top 10 companies were still elevated, but not extraordinarily so. As shown above, market concentration, though very high by recent historical standards, had eased a bit, amidst the backdrop of higher earnings.

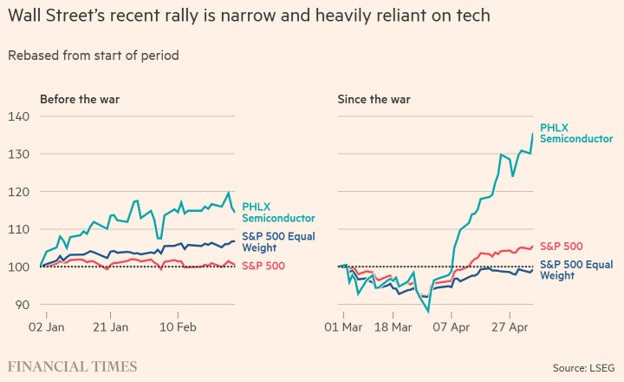

April, however, has seen a reversion back to tech top-heaviness. Emily Herbert, Ray Douglas, and Jonathan Vincent of the Financial Times have charts showing just how the April recovery has been heavily reliant on just a few firms:

Over half of the S&P 500’s gains from April 1st to May 6th have been derived from only five companies. As the authors show below, the equal-weighted S&P 500 index had outpaced the market cap weighted S&P 500 during the first two months of the year, but relative performance has reversed since then:

The authors also cite data indicating that market concentration has reached its highest point since at least 1990.

Heavier market concentration does not necessarily mean that the AI-fueled market surge is ripe for an imminent correction. But it does leave the S&P 500 more vulnerable, as the handful of stocks fueling the continued bull market can easily become the handful of stocks dragging it down.

JMS Capital Group Wealth Services LLC

417 Thorn Street, Suite 300 | Sewickley, PA | 15143 | 412‐415‐1177 | jmscapitalgroup.com

An SEC‐registered investment advisor.

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument or investment strategy. This material has been prepared for informational purposes only, and is not intended to be or interpreted as a recommendation. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice.

‹ Back

Recent Posts

-

Good News, (Potential) Bad News on the Economy

June 5, 2026

-

Are There Rising Interest Rates on the Horizon?

May 29, 2026

-

May Charts and Links

May 15, 2026

-

The S&P 500 Has Reconcentrated

May 11, 2026

-

Iran Blockade… Two Weeks or Two Months?

April 24, 2026