By using our website, you agree to the use of cookies as described in our Cookie Policy

Blog

Quarterly Market Commentary

1Q 2026 - Key Takeaways

The ongoing bull market continued apace for the first two months of 2026 before hostilities in Iran led to an abrupt reversal in March. Whether April’s recovery continues or crumbles depends in significant part on the course of the Iran war, and on the impact and longevity of the effective closure of shipping through the Strait of Hormuz. As this is a quarterly letter, we will primarily focus on market data and events through the end of March, though we will have later thoughts reflecting news that’s accrued in April. Most market areas showed soft but not catastrophic performance, with the S&P 500’s drop of over 4% representing one of the worst performing segments for Q1. Corporate earnings have shown continued strength, suggesting the possibility of a sustained resurgence should the disruption of the Iran war be settled reasonably soon. The Fed has held rates flat—an unsurprising decision, given already elevated inflation combined with the sharp rise in oil prices. Markets currently expect the Fed to hold rates steady until 2027. The macroeconomy still shows reasonable growth, modestly elevated inflation, and moderate unemployment. Much of President Trump’s tariff regime was struck down by the Supreme Court, though the administration may seek to reimpose tariffs under different statutes in the coming months. The major news, obviously, is the Iran war, and while it is not getting worse (as of this writing there is a ceasefire), a resolution does not appear imminent.

The S&P 500 fell 4.4% in Q1 2026, while small caps rose 0.9%. Developed international and emerging markets each posted small losses, sliding 1.1% and 0.1%, respectively, in the first quarter. On the bond side, the US agg was flat in Q1, the 2-year Treasury rate rose 32bp, while the 10-year and 30-year Treasury rates increased marginally.

This middling Q1 performance comes upon the heels of an excellent 2025, during which the S&P 500 rose 17.9%, small caps gained 12.8%, developed international jumped 31.9%, and emerging markets surged 34.2. On the bond side, the US agg rose 7.3% in 2025, while high yield climbed 8.6%, and developed international bonds gained 8.2%.

GDP grew at a 0.5% annualized rate in Q4, while the Atlanta Fed’s GDPnow estimate shows Q1 growth at 1.2%. Both these numbers obviously suggest positive but sluggish growth. Unemployment dipped 0.2% over the past three months, to 4.4%; overall, labor market conditions remained fairly benign, though perhaps somewhat stagnant, as both hiring and firing rates have been low. Core inflation fell in Q1 from 2.6% to 2.5%, and remains modestly above the Fed’s 2% target. After holding rates steady for much of 2025, the Fed made 25bp rate cuts in September, October, and December. However, it kept rates flat during Q1 2026.

At this point, market performance is not nearly on pace to match 2025’s excellence, and the more bullish cases appear increasingly unlikely given the current stalemate in the Iran war and the near-closure of the Strait of Hormuz. Strong earnings amidst a flat quarter means that valuations have become less elevated. AI’s potential is quite high, but markets have already priced in high potential, so the question is whether AI performance can match or even exceed investors’ lofty expectations. Geopolitical risks have mushroomed with the Iran war and the subsequent curtailment of much global shipping. Market recovery in the first part of April suggests a plausible happy ending for 2026, but this outcome likely entails global trade normalizing over the coming months.

1Q 2026 Investment Letter

The first quarter of 2026 may just be an Iran-induced paused in the bull market, or it could be an inflection point signaling more challenging times ahead. GDP growth has slowed but remains positive, unemployment remains under 5%, and core inflation is just 0.5% above target (though headline inflation is rising due to higher oilpric es). The Fed may have limited maneuverability, given already elevated inflation and the potential for further war-induced inflation, but it may feel no need to take action given fairly benign macroeconomic conditions at the moment. Tariffs, even if reconstituted by President Trump, may not be large or broad enough to represent a significant drag on markets or the economy. As with any technological breakthrough, AI has great promise; time will tell on how much it can deliver.

1Q 2026 Market Update

After a promising start to the year, many market areas ended the quarter in flat or negative territory. The S&P 500 fell 4.4%, while the Russell 2000 gained 0.9%. Developed international and emerging markets posted small first quarter losses of 1.1% and 0.1%, respectively. In terms of style, small caps outperformed large caps, while value outperformed growth—small value gained 5.0%, large value added 2.1%, small growth lost 2.8%, while large growth fell 9.8%.

As for sectors, the shock of the Iran war led to a wide dispersion in performance. Energy led the way by far with a 38.2% gain for the quarter, while materials added 9.7%, and utilities rose 8.3%. On the flip side, financials, consumer discretionary, and technology each fell a little over 9%.

Bonds were flat to negative in Q1, as the US agg was flat, high yield bonds fell 0.5%, and international developed bonds plunged 2.7%. Core inflation fell 0.1%, ending the quarter at 2.5%, which is slightly above the Fed’s 2% target, while GDP growth is projected to be positive, albeit under 2%, in Q1. Treasury rates rose moderately in Q1, particularly for shorter-term rates--the 2-year Treasury rate climbed from 3.47% to 3.79%, the 10-year Treasury rate rose from 4.18% to 4.30%, and the 30-year Treasury rate increased from 4.84% to 4.88%. Volatility jumped in March, likely due to the Iran war, but never got worryingly high, as it peaked in the lower thirties.

Update on the Macro Outlook

The economy had been settling into a place characterized by modestly elevated inflation along with a sluggish but largely adequate labor market. Core inflation eased further to 2.5% in Q1; it remains to be seen whether inflation can make the last plunge down to 2% later in 2026. Unemployment has been slowly rising over the past 2-3 years, but peaked at under 5%, and fell slightly to 4.4% in Q1. The US economy isn’t creating as many jobs as it used to, but that’s largely a function of decreased immigration and increased deportations. Payroll growth going forward is likely to continue to be low by historical standards, and expectations should be recalibrated accordingly.

And then President Trump initiated the Iran war, thereby injecting considerable uncertainty into the macroeconomic mix. Although the United States and Israel caused severe damage to Iran’s military and civilian infrastructure, Iran responded by threatening foreign shipping through the Strait of Hormuz. For a time, Iran was able to continue exporting oil at normal levels, while benefitting from higher oil prices. President Trump responded in mid-April by initiating a blockade of Iranian ports.

So the United States and Iran are in a proverbial staring contest. Iran’s ability to export oil, which provides vital funds for its economy, has been significantly constrained. It has a limited ability to store more oil either onshore or offshore; if it runs out of storage space, it would need to shut down some production. Shutting down production typically curtails future yields of oil fields, so that a shutdown damages future income as well as current income. The hope of the Trump Administration is that facing permanent losses of billions per year in oil revenue, Iran will blink and largely acquiesce to Trump’s terms. Some projections have Iran facing production shutdowns in as little as two weeks, or roughly by the end of April.

On the other hand, the Iran war is already unpopular in the United States, gas prices have risen considerably, and the downstream consequences are already likely to affect the midterm elections—normalization of shipping and oil prices is likely to take months, even if a comprehensive agreement were reached within days. If Iranian leadership feels their survival is at stake, it may be motivated to prolong the stalemate, in the hopes that accumulating economic damage will lead Trump to back down.

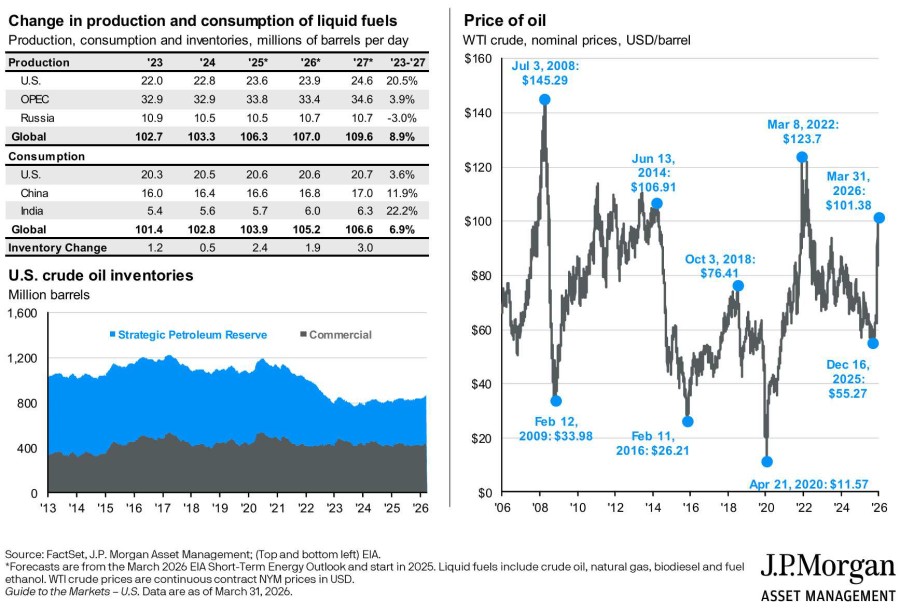

For now, oil prices, while much higher than they were a year ago, are not eye-popping by historical measures:

Oil prices were higher in the immediate aftermath of Russia’s invasion of Ukraine, and since then, global production has risen significantly. Many countries have also been utilizing their petroleum reserves to compensate for the reduced oil coming from the Persian Gulf. Given that oil demand is fairly inelastic in the short-term—most people will continue driving to work even in the face of higher gasoline prices—we seem to be in a race against time, seeing which will happen first—will Iran’s economy weaken sufficiently to the point where Iran will be desperate to cut a deal, or will the global economy burn through enough fuel reserves and easy adaptations that we will have to see oil demand destruction—in other words, the sharply rising prices necessary to bring demand into line with limited supply.

Amidst this backdrop the Fed is expected to hold rates steady until 2027. The Fed may be reluctant to cut rates in the face of rising headline inflation risks amidst already above-target inflation. It may be reluctant to raise rates giving the economic pain accumulating from the Iran war. It may simply adopt a wait and see approach—to see if the Strait of Hormuz is reopened to traffic soon, or to better understand some of the economic fallout should it remain closed in the coming months.

Portfolio Positioning and Closing Thoughts

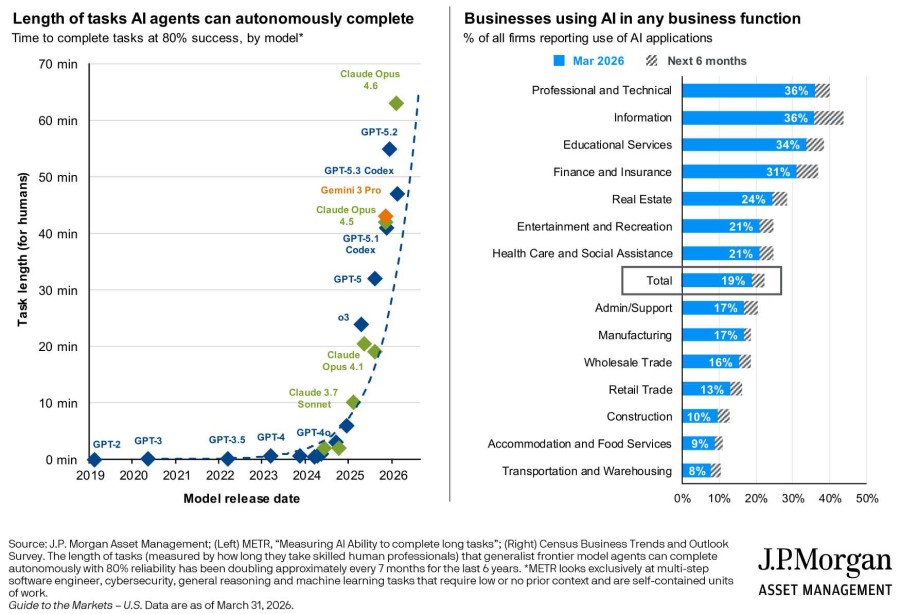

For all the concern we’re expressing about the consequences of the Iran war, it may be relatively small potatoes for markets when compared to the AI juggernaut. JPMorgan has a chart detailing AI’s progress and adoption by businesses:

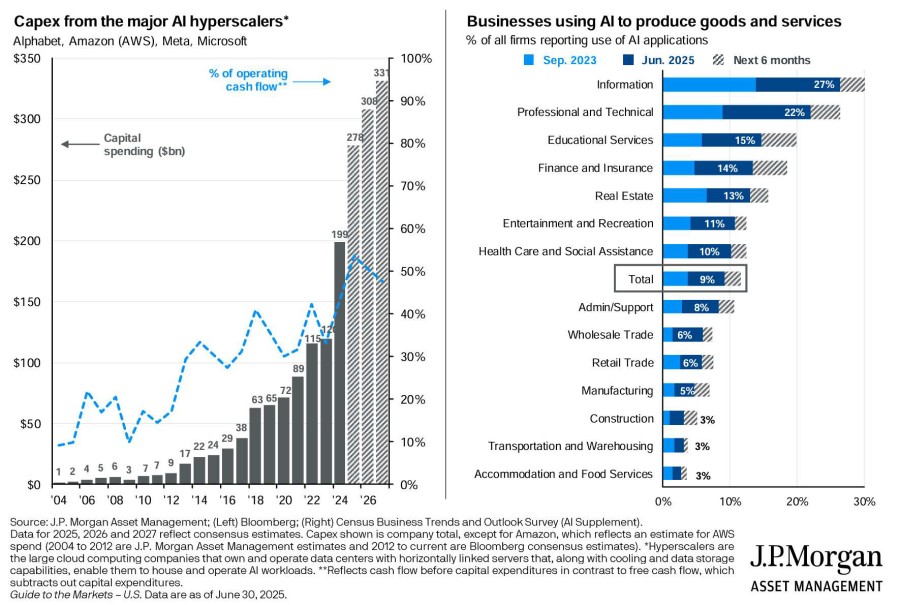

Capabilities of AI agents have been growing exponentially over the past two years. AI adoption by businesses has already reached 19%. To provide some further context we went back and pulled a similar JPMorgan chart from just 9 months ago:

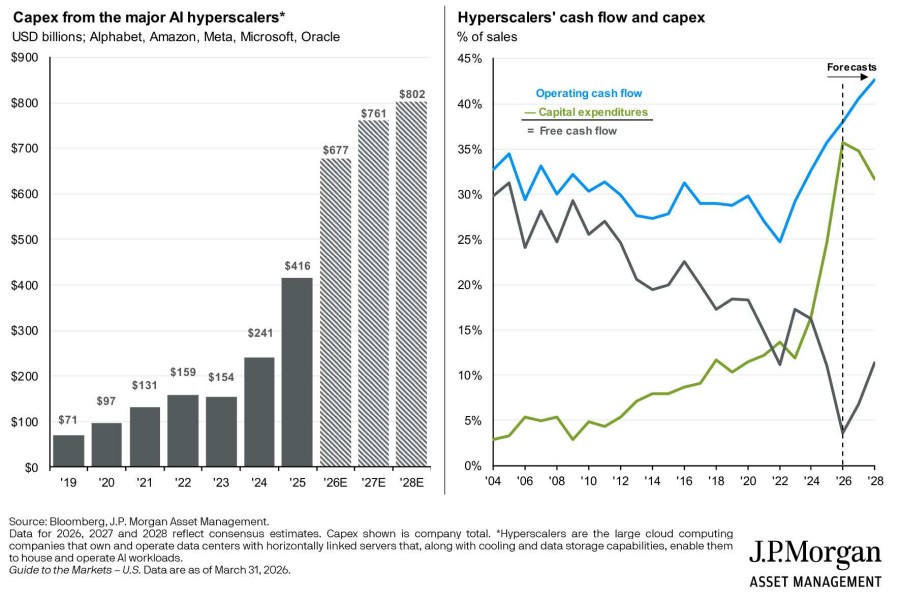

AI adoption has grown from 9% to 19% in 9 months. One chart won’t provide a complete picture of how AI will impact businesses, but the speed with which AI is permeating businesses is astonishing. Spending on AI is also growing at an amazing pace. The chart above, which in 2025 projected about $300 billion in capital spending in 2026, became outdated in months—here is JPMorgan’s newest chart (with Oracle added to the list of hyperscalers):

Projected spending has more than doubled in the last nine months. As we write this the S&P 500 has recovered its losses and reached new record highs in April, largely due to tech stock bounceback.

The first quarter of 2026 saw several points of inflection. The start to the year was generally solid – with the S&P 500 Index up close to 2.5% by late January. In a bit of a sentiment shift, large value stocks outperformed large growth stocks by nearly 4% in the period. Strength in financials, energy and cyclicals drove the market while multiple compression and mild concerns over AI capex weighed on technology companies. Sentiment surprisingly shifted to small cap stocks as well during the period as the cheaper stocks – which are less focused on long-duration growth assumptions - rallied on a relative basis. Additionally, international stocks continued to enjoy relative performance wins over U.S. large caps for the quarter. Less reliance on mega-cap technology stocks provided less of a concentration drag for foreign stocks. Higher cyclical exposure helped as well. The gap in performance will likely close in the coming quarters. While small caps are enjoying some short-term success,

we are not adding to our exposure in the asset class, and some economic realities may put pressure on those stocks later in 2026. With that said, valuations remain attractive. The same can be said for foreign stocks. Even after a stellar 2025 in terms of returns, we believe there is more room to run considering their decade-plus underperformance versus U.S. large caps. The direction of the dollar was a headwind for foreign stocks in Q1, but only a 1%-2% impact in general. This can swing back in favor of foreign stocks quite easily.

The conflict in Iran, while moving the market lower in general, was a wind at the back of energy stocks. The sector witnessed a return of over 38% for the quarter – far ahead of the next best sector, materials. The sectors where the Magnificent 7 stocks reside – Information Technology, Communication Services and Consumer Discretionary – were the hardest hit for the quarter. A combination of pressure from rising yields and profit taking on the back of a strong 2025 drove the decline in those areas. We would expect to see a bounce in the growth side in the short-term. However, if the conflict in Iran drags through the remainder of 2026, the promise of AI might not be enough to offset the reality of rising inflation and higher yields. While the stock market has found its feet in April as the ceasefire with Iran has calmed some nerves, we would expect a continued backand-forth in the coming months.

Bonds felt the pressure of rising rates early in 2026. The flat return for core bonds was a headwind for diversified portfolios as these equity ballasts did not help to offset stock losses. We would expect some other periods of pressure from rising rates on duration heavy assets in the coming quarters. Credit held up better than duration to start 2026. Despite the conflict in Iran and negative headlines around certain areas of private credit, credit spreads did not blow out during the quarter. Higher starting yields across the board helped to offset the negative price movement in many fixed income areas. Emerging market debt outpaced most fixed income asset classes for the quarter, helping diversified bond portfolios. We are mildly concerned with the direction of interest rates in the short to intermediate-term. We prefer higher exposure to shorter-term bonds, where we can depend on decent yields with less volatility, paired with a diversified basket of multi-sector fixed income strategies (including emerging market portfolios).

—JMS Team

JMS Capital Group Wealth Services LLC

417 Thorn Street, Suite 300 | Sewickley, PA | 15143 | 412‐415‐1177 | jmscapitalgroup.com

An SEC-registered investment advisor

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument or investment strategy. Certain material in this work is proprietary to and copyrighted by Litman Gregory Analytics and is used by JMS Capital Group Wealth Services LLC with permission. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. Any references to future returns are not promises - or even estimates - of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation for a specific investment. Past performance is not a guarantee of future results.

With the exception of historical matters, the items discussed are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. We have based these projections on our current expectations and assumptions about current and future events - as of the time of this writing. While we consider these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond our control. There can be no assurances that any returns presented will be achieved.

‹ Back

Recent Posts

-

Good News, (Potential) Bad News on the Economy

June 5, 2026

-

Are There Rising Interest Rates on the Horizon?

May 29, 2026

-

May Charts and Links

May 15, 2026

-

The S&P 500 Has Reconcentrated

May 11, 2026

-

Iran Blockade… Two Weeks or Two Months?

April 24, 2026