By using our website, you agree to the use of cookies as described in our Cookie Policy

Blog

Q3 2017 Market Commentary

Third Quarter 2017 Key Takeaways

Despite its reputation as the worst seasonal period for stocks, global stock markets rallied again. Emerging‐market stocks were strongest, surging 8%, followed by European stocks, which gained 6.2%. More broadly, developed international stocks rose 5.5%. For the third consecutive quarter, the U.S. dollar depreciated against foreign currencies, boosting dollar‐based investor returns in these markets.

Our portfolios have benefited over the past year from the very strong relative and absolute performance of international and emerging‐market stocks. Yet foreign stocks continue to look very attractive relative to U.S. stocks and offer solid absolute expected returns. Even with this strong performance, the price‐to‐earnings ratio for international stocks has actually fallen in 2017 due to earnings growth outpacing price appreciation.

The U.S. market delivered strong returns in the third quarter, extending its winning streak to eight consecutive quarters and a remarkable 18 out of the last 19 quarters. The S&P 500 Index closed at an all‐time high, gaining 4.5%.

Within the U.S. market, larger‐cap growth stocks—technology stocks in particular—continued their year‐to‐date dominance over smaller‐cap and value stocks, a sharp reversal from what we saw last year. Looking at industry sectors, energy stocks had a big rebound as oil prices rose above $50. But for the year, the sector is still down 6.6%, while technology and health care have soared 27% and 20%, respectively.

One indicator of how calm the stock market has been this year is that its largest decline (drawdown) has been a loss of 2.8% (from March 1 to April 13). Going back to 1929, there has been only one calendar year when the largest drawdown was smaller than that, according to Ned Davis Research.

Moving to the fixed‐income markets, core investment‐grade bonds inched up 0.7% for the quarter. The 10‐year Treasury yield (which moves inversely to bond prices) ended the quarter flat, but this masked intra‐quarter shifts. It bottomed in early September as fears over North Korea, hurricanes, and political events peaked. But the yield shot up into month‐end, closing the quarter right about where it stood three months earlier.

Credit‐sensitive (higher‐risk) sectors of the fixed‐income market outperformed core bonds for the quarter. The high‐yield bond index gained 2% and floating‐rate loans were up 1%. Our portfolios have also benefited from exposure to actively managed, absolute‐return‐oriented bond funds, which again outperformed core bonds overall this quarter.

In this quarter's commentary, we highlight a few of the positive economic indicators in support of a synchronized global growth recovery. But, as always, there are significant uncertainties and “unknowables” when it comes to economic forecasting. Humility and intellectual honesty—knowing what you don’t know and what you can’t know and can’t accurately predict—are crucial. Stock market corrections can happen any time despite the global economy’s current health, and investors should prepare themselves for market dips and drops along the way.

Third Quarter 2017 Investment Commentary

For the quarter, our globally diversified balanced portfolios generated attractive returns as all the major asset classes registered gains for the period. Our portfolios particularly benefited from their exposure to emerging‐market and developed international stocks, both of which had strong absolute returns and also beat U.S. stocks.

Update on the Macro Backdrop

The synchronized global economic recovery that we wrote about in the first quarter continues apace, providing a solid foundation for corporate earnings and financial assets in general. Below we highlight a few of the positive global economic indicators:

- The OECD Composite Leading Indicator recently hit its highest level since October 2014, and growth is broadly distributed across OECD countries, reflecting a healthy global expansion.

- In August, the Global Manufacturing Purchasing Managers Index (PMI) hit its highest level in over six years. Eurozone and Emerging Market PMIs also rose to multiyear highs.

- Easing inflationary pressures in emerging markets have allowed numerous emerging‐market central banks to lower interest rates this year, which is typically positive for local stock markets.

- Real GDP growth in the United States remains subpar by historical standards but continues to grind along at around a 2% annual rate.

- Financial conditions have eased over the past year, despite the Federal Reserve’s three rate hikes; this could bode well for economic growth over the next few quarters at least.

- Finally, global central bank policy remains accommodative and stimulative.

Still, there is disagreement and debate among economists and strategists as to whether inflationary or deflationary risks should be paramount for investors at this point in the cycle, and related to that, whether Fed policy is too dovish or hawkish. It bears repeating that there are significant uncertainties and “unknowables” when it comes to economic forecasting. As such, we always consider a range of potential scenarios in our investment decisions and portfolio management rather than betting heavily on any single macro forecast. As the proverb goes, “It’s difficult to make predictions, especially about the future.”

Asset Class Performance & Investment Outlook

U.S. Stocks: As noted earlier, the near‐term macroeconomic (fundamentals) backdrop for U.S. stocks still looks pretty solid. But U.S. stocks have high valuation risk. Across almost every absolute valuation metric, U.S. stocks look expensive to very expensive.

As such, in our base case scenario, we expect the market price‐to‐earnings (P/E) multiple to decline toward historical norms over the next several years. If this happens, it will be a drag on total market returns. Effectively, this would reverse some (but not all) of the large positive impact the sharp P/E multiple expansion has had on market returns over the past five years.

In our assessment, this argues for caution when it comes to U.S. stocks, looking out over the next five‐plus years. That is why we remain somewhat underweight to U.S. stocks, despite what may continue to be a supportive macro backdrop for them over at least the next few quarters.

Foreign Stocks: International and emerging‐market stocks have generated strong relative and absolute performance over the past year. Part of this performance can be explained by the euro’s sharp 12% appreciation against the U.S.dollar in 2017. Consequently, the euro/dollar exchange rate now looks to be in a broad fair value range, with the euro now only slightly undervalued. Therefore, looking ahead over a multiyear time horizon, we wouldn’t count on additional meaningful gains from the currency.

However, based on our analysis, foreign stocks still look very attractive relative to U.S. stocks, and offer solid absolute returns, in the mid‐ to upper‐single‐digit range, at least, over our tactical investment horizon in our base case scenario.This compares to the zero to low single‐digit returns we expect from U.S. stocks in our base case. Therefore, we remain overweight to developed international and emerging‐market stocks.

In Europe and the emerging markets, we are seeing the corporate earnings (and stock market) recovery we have been expecting. Yet, earnings remain far below their pre‐crisis highs and also below what we view as their normalized (longer‐term) trend growth level. Absolute valuations remain reasonable if no longer depressed.

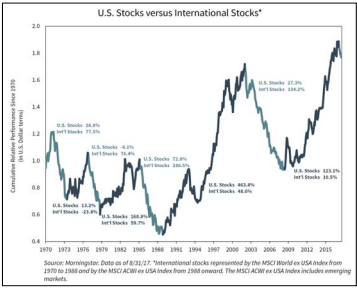

The relative strength chart to the right shows that U.S. stocks’ large return advantage since the financial crisis has only begun to reverse. As we’ve written before, and financial market history

demonstrates, asset classes go through cycles of relative performance—driven not just by their underlying economic fundamentals but by human herd behavior and market sentiment that swing to

excess. We may be in the early stages of the pendulum swinging back in favor of foreign stocks. While we can’t predict short‐term swings in sentiment, our forward‐looking analysis of the

fundamentals and valuations certainly supports that view.

Fixed‐Income: Within the fixed‐income portion of our balanced portfolios, our long‐established positions in several flexible and absolute‐return‐oriented bond funds added value again for the quarter. These funds are also ahead of the core bond index for the year.

Alternative Strategies: Our liquid alternatives investments continued apace to fulfill their mandate of 4%‐6% annual growth. In the third quarter, most of our alternative funds provided positive, steady returns in the 0%‐2% range. The one outlier was in a positive direction, as long‐short equity posted strong gains over the past three months. Conversely, managed futures, which has struggled this year, stayed flat for the quarter, though its uncorrelated returns still may offer downside protection for the portfolio. Overall, the diversifying positions of our liquid alternatives outperformed the core bond index, as represented by the US Agg, but lagged global equities.

Closing Comments

Despite the U.S. economy’s rather healthy economic indicators, it’s worth noting that a typical 5% to 10%‐plus stock market correction can happen at any time, triggered by any number of unpredictable and/or unexpected events.Historically, the U.S. market has dropped at least 5% roughly three times a year and declined 10% or more about once a year. We are at 330 days and counting since the last 5% drop; this is the longest such streak in 26 years. Given that historical reference, the U.S. market seems long overdue for a correction.

However, a true bear market in U.S. stocks (a sustained 20%‐plus decline) is almost always associated with an economic recession. Absent a recession, a bear market is unlikely. Recessions, in turn, are typically caused by excessive Fed tightening, usually in response to inflationary pressures, an overheating economy, or financial market excesses, none of which seem imminent in the U.S. or global economy. So although this is now the third‐longest economic expansion and second‐longest bull market in U.S. history, neither appears ready to die of old age just yet.

If that’s the case, then we expect to continue to benefit from our exposure to international and emerging‐market stocks as their performance “catches up” to U.S. stocks. We also expect our flexible fixed‐income to outperform the core bond index, due to their yield advantage and lower duration (which mitigates the negative price impact from rising interest rates). Lower‐risk alternative strategies should also perform relatively well in that environment, although they may lag stock returns.

But as the cycle turns, the likelihood of a recession increases. We’d say one is very likely within the next five years, and a bear market as well. Our five‐year base case scenario assumes that will happen. Our portfolios will have exposure to risky assets that will be hit hard by a recessionary bear market—although the degree of exposure depends on the individual portfolio’s risk objective. Investors must be prepared—psychologically and financially—for market dips and drops along the way. They are inevitable and may be unsettling, but they are also temporary.

It’s also important to remember that the next bear market will surely create some table‐pounding tactical investment opportunities, as many risky asset classes will get excessively beaten down in price relative to their longer‐term fundamentals. Given our positioning in lower‐risk asset classes, especially absolute return focused alternative strategies, we expect to be able to take advantage of such opportunities.

In the meantime, we have built balanced portfolios that are resilient across a range of scenarios; diversified across investment strategies, asset classes, and risk exposures; and tilted to the areas our analysis indicates currently have the most attractive risk/return profiles, such as developed international stocks, emerging‐market stocks, absolute‐return‐ oriented and flexible bond funds, and lower‐risk liquid alternative strategies.

Thank you for your continued confidence and trust. —JMS Team

Disclosure:

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument or investment strategy. Certain material in this work is proprietary to and copyrighted by Litman Gregory Analytics and is used by JMS Capital Group Wealth Services LLC with permission. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. Any references to future returns are not promises ‐ or even estimates ‐ of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation for a specific investment. Past performance is not a guarantee of future results.

With the exception of historical matters, the items discussed are forward‐looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. We have based these projections on our current expectations and assumptions about current and future events as of October 2017. While we consider these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond our control. There can be no assurances that any returns presented will be achieved.

‹ Back

Recent Posts

-

Quarterly Market Commentary

August 4, 2026

-

Good News, (Potential) Bad News on the Economy

June 5, 2026

-

Are There Rising Interest Rates on the Horizon?

May 29, 2026

-

May Charts and Links

May 15, 2026

-

The S&P 500 Has Reconcentrated

May 11, 2026